Income Splitting Canada: New Income Splitting Rules (TOSI)

‘Income Splitting’ refers to the ability of a business owner to ‘sprinkle’ bits of income to various members of his or her family including children, brothers, sisters and parents, so as to reduce that business owner’s overall tax obligation.

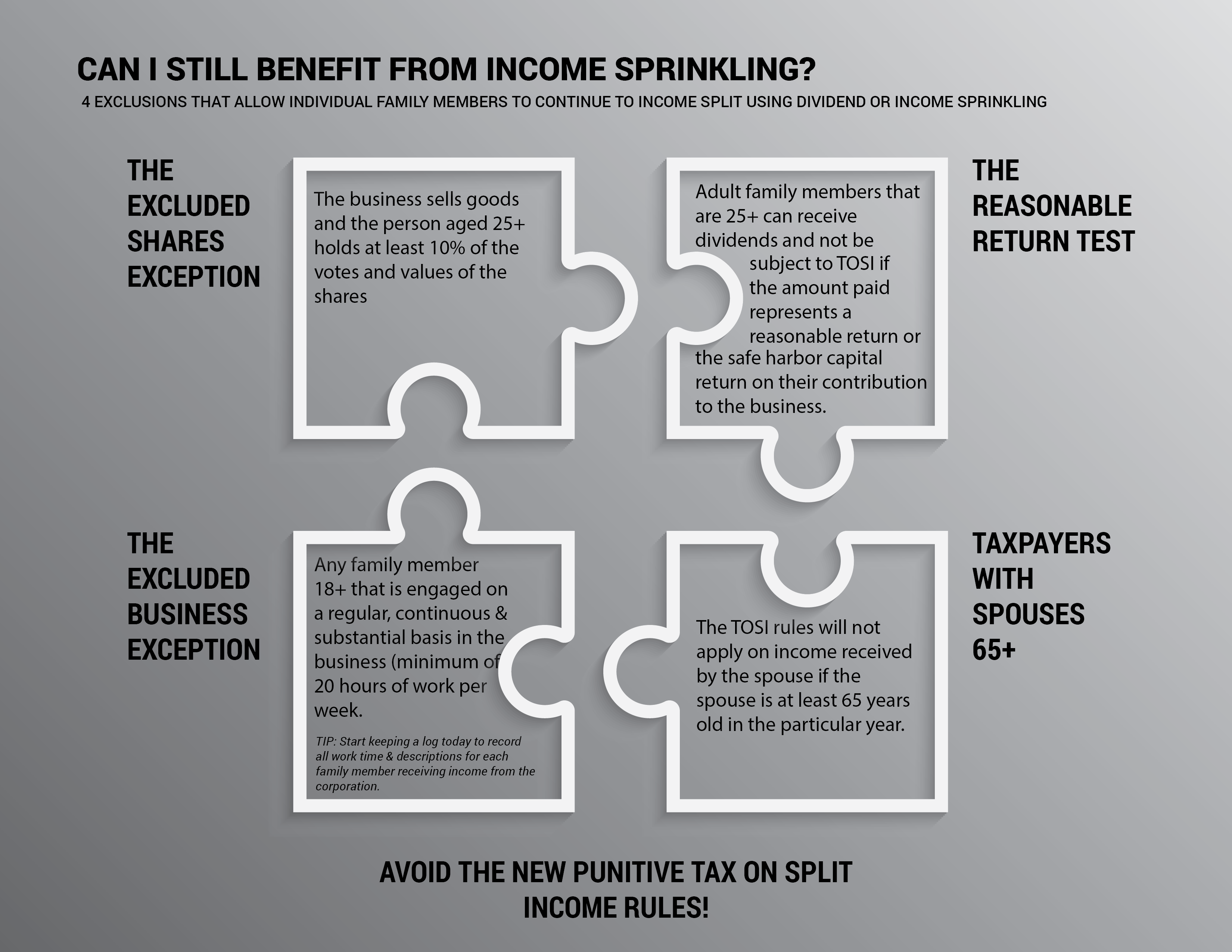

Tax Savings Through Creative Income Sprinkling

While traditional income sprinkling opportunities were fundamentally changed and largely eradicated by the overhaul to corporate tax planning by the Liberal government in 2017, some formidable tax planning opportunities are still available to Canadians.

Tax Planning and the General Anti-Avoidance Rule (“GAAR”)

A taxpayer is entitled to arrange his affairs in such a way that results in the lowest amount of taxes payable. However, our right as Canadians to tax plan is not unfettered.

Salary or Dividends? Which is the best way to receive compensation as the owner of a corporation?

Which one is best? The one that results in a “tax rate advantage”; that is, the compensation model whereby the total corporate and personal tax paid on one form of compensation (either dividends or salary) is less than the corporate and personal tax paid on the other form of compensation.

Tax Free Inter-Corporate Dividends

Inter-corporate dividends refer to dividends that are paid by one company to another company holding shares in the first, particularly where the companies are operated by the same person or group of people (as with a holding company structure).