Salary vs. Dividends? Which is the best way to receive compensation as the owner of a corporation in Canada?

You are the owner of a small business corporation in Canada and want to pay as little tax as possible on both the corporate level and at the personal income level. With that in mind, you are wondering whether it is best to pay yourself in the form of a salary vs. through dividends.

Which one is best? The one that results in a “tax rate advantage”; that is, the compensation model whereby the total corporate and personal tax paid on one form of compensation (either dividends or salary) is less than the corporate and personal tax paid on the other form of compensation.

Figuring out whether to get paid in dividends, by salary or a combination of both depends on a variety of factors: these include the amount earned inside the corporation, personal income levels, future considerations such as one’s retirement needs or desire to build one’s credit for the purchase of a big-ticket item, ability to defer payment to future years, and income sprinkling potential.

Pros and Cons of Receiving a Business Salary

Basically, paying yourself with a salary means that you save at the corporate level but pay more at the personal level. Why? Because salaries are fully deductible at the corporate level, while the tax rate on income is higher than the tax rate on dividends. Along with the higher tax rate, however, there are distinct advantages that help to offset your tax burden.

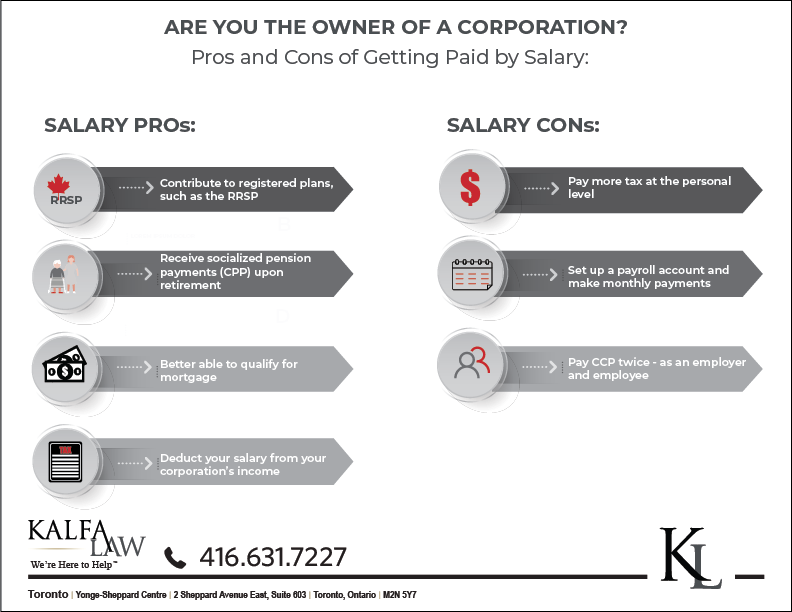

Receiving a salary as a business corporate owner comes with the following advantages:

- Receiving a salary allows you to contribute to your registered retirement savings plan (RRSP) or a tax free savings account (TFSA)

- Receiving a salary allows you to receive tax credits, such as the child tax benefit

- Receiving a salary means you pay into EI (employment insurance) and CPP (Canada Pension Plan) which may be valuable social safety tools in the event you are without a job or plan on relying on CPP for retirement

- Paying with a salary and/or bonus is a tax deduction for your corporation

- Paying a salary does not require net taxable income – you can pay yourself a salary where the business is not profitable.

The disadvantages to paying yourself with a salary are the following:

- Higher tax rate on personal income than dividends.

- Having to set up a payroll account and make payments, along with source deductions, every month; failure to do so will result in stiff penalties.

- Paying mandatory Canada Pension Plan (CPP) twice: once as an employer and again as an employee.

To recap, while tax rates on personal income are higher, there are other benefits to choosing to receive salary combined with the tax savings on the corporate level.

Pros and Cons of Paying Yourself with Dividends

Paying yourself in dividends means more tax at the corporate level and lower tax on the personal level. Why? Because, unlike salaries which are deductible since they are drawn from the gross revenue or top line of a business’s income, dividends are drawn from retained earnings which are after-tax profits, which are not deductible to the corporation. On the up side, when you receive the funds, dividends are taxed at a lower rate compared to salaries due to the Dividend Tax Credit (DTC) mechanism.

Receiving dividends as a business corporate owner comes with the following advantages:

- Dividends are taxed at a much lower rate than are salaries; the business owner will pay a lot let less

- You can defer taking dividends to another tax year when it is more advantageous if you don’t need the money to live on

- You can take dividends at any time without the hassle of setting up a payroll account and making monthly payroll payments

- Dividends are gross income in the sense they face no tax before payment to you. You pocket the funds and pay the tax at tax time.

Receiving dividends come with the following disadvantages:

- You will not be making regular payments into a retirement or pension plans (CPP or RRSP) or tax -free savings accounts (TFSA)

- You will not be making regular contributions to EI or CPP which may be useful social safety income methods

- You will not be able to claim personal income tax deductions or expenses

As indicated earlier, there are various considerations to take into account and there is usually no one way of paying yourself that will result in a “tax-rate advantage.” What is optimal will likely be a combination of both salary and dividends.

The first consideration when making the decision as to how to pay yourself is to minimize the tax burden inside of your corporation. Particularly, you want to maximize the amount of income subject to the SBD rate of 12.5% tax. The SBD is available on the first $500,000 of net profit and so one is inclined to maximize deductions inside a corporation in order to make the $500,000 net limit stretch as far as possible. While this will involve paying higher taxes on the personal level, your tax rate can be offset through tax planning tools such as claiming expenses.

If your small business has earned less than $500,000 regardless of its deductions, it might be best to pay yourself in dividends (or a combination of salary and dividends) because of the lower tax rate. If you don’t need the money to live on in the current year, you can choose to take dividends in a future year, which will yield a “tax deferral advantage” since you will only be paying tax on the funds you need to support your lifestyle each year and no more. The difference between the corporate tax, which has to paid each year, and personal tax of dividends, which can be deferred, can be reinvested within the corporation to earn additional income until the dividend is ultimately paid, possibly many years later.

Because every business owner’s needs and goals are different as are the profiles of corporations, it is best to consult with an experienced tax lawyer who will come up with the perfect combination of compensation models to maximize the wealth of both your corporation and your personal portfolio.

Contact a lawyer at Kalfa Law Firm to help you with your tax needs. You work hard for your money; we work hard for you to keep it.

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law Firm 2020