Capital Gains Exemption: Everything You Need To Know

Here’s everything you need to know about the capital gains exemption in Canada:

Who doesn’t want to reduce their tax burden? Smart tax planning involves understanding the conditions that qualify you for an exemption, how much of an exemption you qualify for, and what you can do to ensure that you do qualify. One of the most utilized exemptions is called the “Lifetime Capital Gains Exemption.”

The Lifetime Capital Gains Exemption (LCGE) pertains to the amount of profits from a sale, otherwise known as capital gains, which are shielded from tax. But before we look at the ins and outs of this exemption, let’s begin with an understanding of what a capital gains tax is.

What is a capital gains tax?

When you sell certain assets, the money that you make is part of your income and is subject to what is called a “capital gains” tax.

Making a profit from the sale of a capital asset includes the sale of tangible and intangible items, such as stocks, bonds, precious metals, cars, boats, and land and real estate properties.

So how much tax do you have to pay on capital gains?

Currently, 50% of realized capital gains are taxable in Canada. Let’s look a simple example. Let’s say you sold your diamond ring and earned a profit (capital gains) of $10,000. You are taxed on $5000 at your marginal tax rate. That is, if you were in the top tax bracket and your profit was $10,000, you would be taxed on $5000 at 53.53 percent, in Ontario. A formula for this example using the top tax bracket would be as follows:

(Capital gain x 50.00%) x marginal tax rate = capital gain tax

($10,000 x 50.00%) x 53.53% = $5000 x 53.53% = $2,676.50

In this example your capital gains tax on $10,000 is $2,676.50, leaving you with $7323.50.

What is a capital loss and how can that help to reduce your tax burden?

A capital loss occurs when you sell an asset and lose money. You can use that to your advantage to pay less of a capital gains tax that year.

Let’s say that you bought a building for $100,000 and sold it for $95,000. Your capital loss would be 5,000. Putting it all together, your capital gain on the sale of your diamond was $10,000, while your capital loss on the sale of your building was $5,000, giving you a net capital gain of $5000 that would be taxed at your marginal tax rate.

By using your capital loss to offset your capital gains, instead of paying $2,150 in capital gains tax on the profit you made on the sale of your diamond, you will pay half that at $1,075, leaving you with $8,925 in profit instead of $7,850.00.

Your capital losses can be carried forward indefinitely to offset future years’ capital gains; capital losses not used in the current year can also be carried back to the previous three tax years to offset capital gains tax paid in those years.

To summarize, for corporations and individuals, 50% of realized capital gains are taxable (called the capital gains inclusion rate). The net taxable capital gains (which is calculated as 50% of total capital gains minus 50% of total capital losses) are subject to income tax at normal corporate tax rates.

While capital losses can reduce an individual or corporation’s tax burden, there are better ways to minimize the amount of tax one must pay on a capital gain. Let’s now look at the “lifetime capital gains exemption”.

What is a Lifetime Capital Gains Exemption?

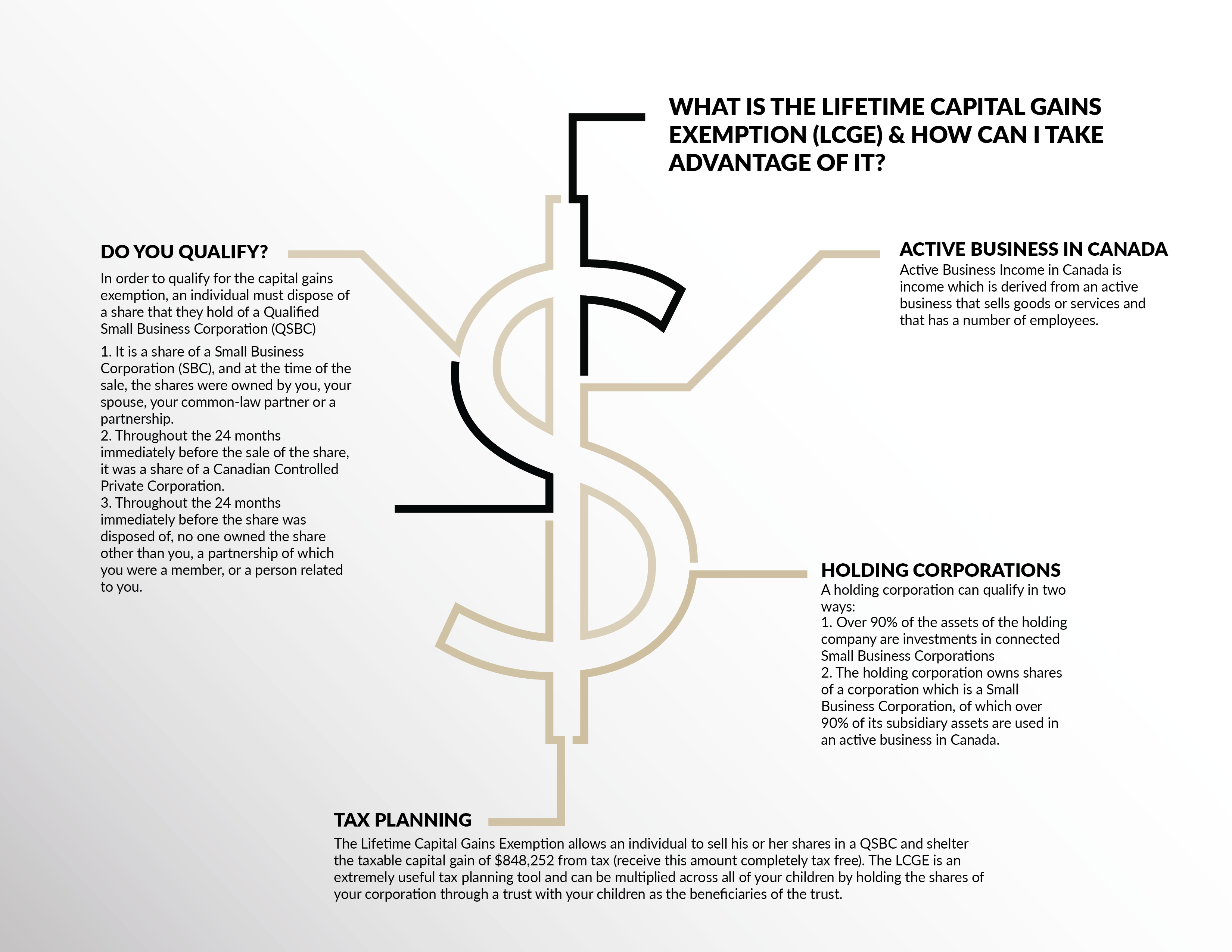

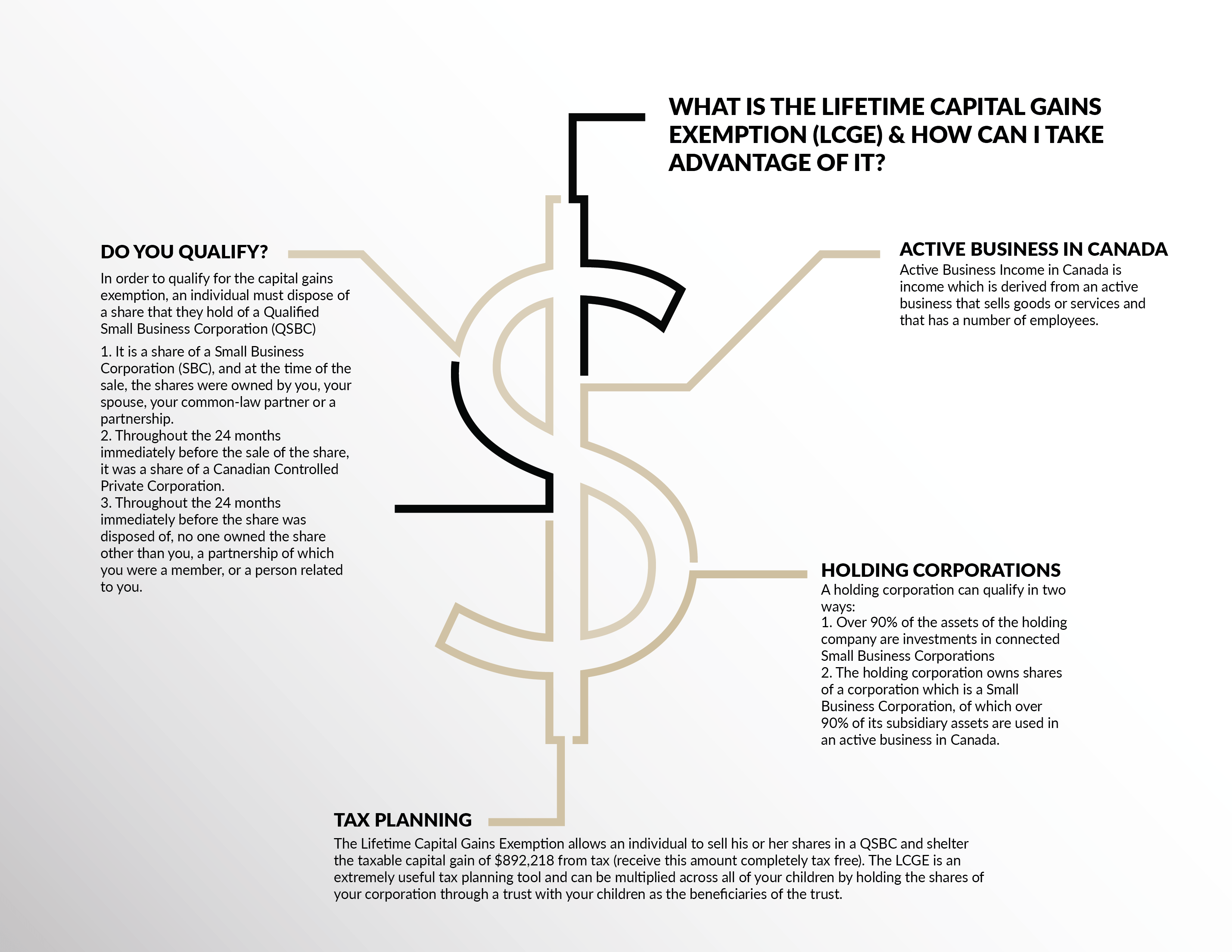

A lifetime capital gains exemption (LCGE) is an exemption on capital gains tax on the disposition of shares of a qualified small business corporation.

Generally, when a taxpayer disposes of capital property—such as corporate shares—and realizes a capital gain, the taxpayer must include one-half of the gain in his or her income. But if the disposed property is either a qualified small-business-corporation share (QSBC share) or qualified farm or fishing property, the gain may be deductible.

The LCGE in 2021 is $892,218. This means that an individual can sell his or her shares in a qualified small business corporation and shelter $892,218 of capital gains from tax (meaning receive this amount completely tax free). The threshold cap is indexed to inflation, increasing incrementally each year according to the Consumer Price Index. For the list of pegged personal income tax and benefit amounts for 2021 set out by Canada Revenue, Click Here.

Qualifying for the LCGE

Only individuals—as opposed to corporations—qualify for the LCGE. To qualify, an individual must be a resident in Canada throughout the tax year in which the individual claims the deduction.

As we discussed, another important qualifier is the nature of the small business corporation.

What is a Qualified Small Business Corporation (QSBC)?

The Income Tax Act provides a complex definition of a QSBC share. But, at bottom, a qualified small-business-corporation share must meet three requirements:

- The share must be that of a “small business corporation,” which is a Canadian-controlled private corporation using at least 90% of its assets in an active business in Canada at the time of disposition.

- Only the individual claiming the LCGE or an individual, partnership, or corporation related to the individual, must own the QSBC share throughout the 24 months preceding the share’s disposition.

- Throughout the 24-month period preceding the QSBC share’s disposition—that is, during the period that either the claiming individual or a related person owned the share—the share was that of a Canadian-controlled private corporation using at least 50% of its assets in an active business in Canada.

Do Holding corporations Qualify for the LCGE?

Holding corporations qualify for the LCGE if over 90% of its investments are in a qualified small business corporation or if it owns shares in a small business corporation that satisfies the conditions discussed above:

- At the time of the disposition of shares, over 90% of the holding corporation’s assets are involved in an active business in Canada.

- Over 50% of the holding corporation’s assets were in an active business in Canada in the preceding 24 months.

- The qualifying shares must be owned by the corporation in the preceding 24 months.

Tax Planning – Purify the Corporation

Qualifying for the LCGE can only work if you meet the 90% or 50% threshold. That is a high bar to satisfy. Thankfully, there are tax-planning strategies available to small business corporations that can help them to meet these thresholds.

One is called “purifying the corporation.” Purification involves taking action to dispose of or change the structure of the corporation so that it is stripped of certain assets that are not being actively used in the business. This can be done by transferring the assets to a newly formed corporation under s.85 of the Income Tax Act, which rolls over the assets on a tax neutral basis (no tax is paid on the transfer).

Make sure that you take advantage of all the tax saving possibilities by working with a qualified tax lawyer. For more information on the LCGE and whether your corporation may qualify, Contact Us.

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law Firm 2021

The above provides information of a general nature only. This does not constitute legal advice. All transactions or circumstances vary, and specified legal advice is required to meet your particular needs. If you have a legal question you should consult with a lawyer.