Tax Elections that Cancel GST/HST on the Sale of Assets

Section 156(1) of the Excise Tax Act (Asset Purchase) – Form RC4616

In our last article, we looked at Election 167(1), which permits the sale of a business’s personal property on a tax free basis provided certain conditions are met. Personal property refers to any movable or intangible item owned that is not recognized as “real” property, the latter referring to land, any buildings on that land, and anything attached to that land, the sale of which does not qualify for Election 156.

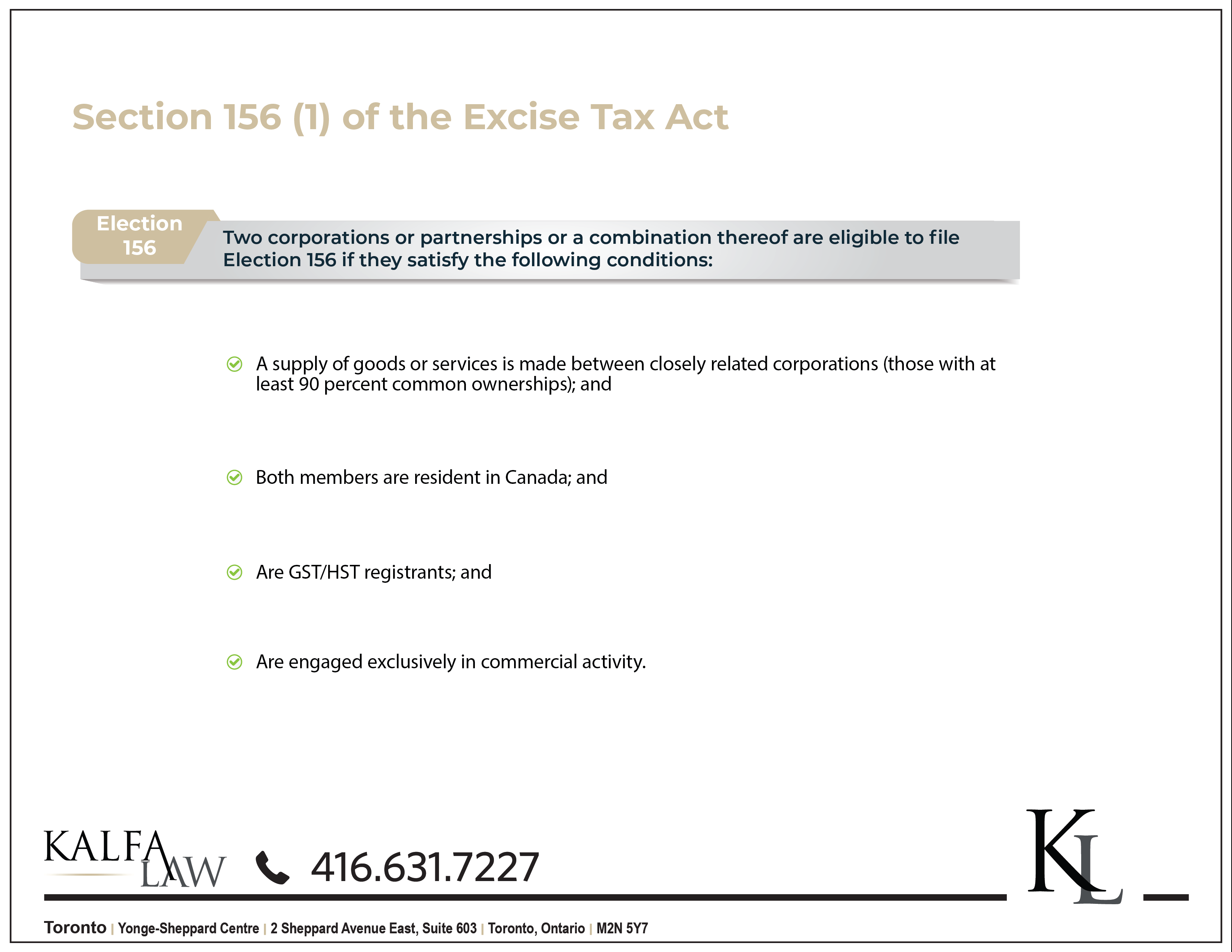

But what if these conditions do not apply? Are there any other tax elections that can be utilized to nullify payable GST/HST on the sale of supplies? Absolutely. Let us look at Election 156, under the Excise Tax Act, which effectively provides zero-rate of tax on the transfer of assets within a closing related group, provided that certain conditions are met. An election under s.156 may permit the supply to be made at NIL consideration for the purpose of the GST/HST.

Generally speaking, the conditions require that the supply of goods is made between closely related corporations or partnerships or a combination thereof, where there is at least a 90% interest in the other corporation or partnership or at least 90% ownership of the other corporation’s or partnership’s shares. Where there is this degree of relationship, we deem the parties to be “closely related” and therefore constitute a “qualifying group.”

Example

For example, if Acme Corporation owns a 95% interest in Biology Inc, then they are closely related and constitute a qualifying group for the purpose of qualifying for election 156, which will provide a zero-rate of tax on the transfer of assets from Acme to Biology Inc.

Application of the Rule under s156

Similarly, the rule applies between a corporation or partnership that is a member of a qualifying group of which the particular corporation or partnership is a member. For example, if Canadian partnership A has a 95% interest in Canadian partnership B, then they form a qualifying group. Canadian partnership B, in turn, holds a 95% interest in Canadian partnership C, forming a qualifying group of which Canadian partnership A is a member. Therefore all three partnerships form a qualifying group, which would allow a zero-rate of GST/HST on the sale of assets made between any of two of the three partnerships.

Other conditions require that both members are residents in Canada, both are GST/HST registrants and both are engaged exclusively in a commercial activity.

The Sale of Real Property

WhileETA section 156 does not apply to sale of real property, section 221 of the ETA provides relief if the purchaser is a registrant. Under section 221, the obligation to remit GST/HST on the sale of real property falls on the purchaser alone. Another election requires that the purchaser self-report the payable GST / HST. The taxable real property must be intended to be used 50% or more in taxable activities to be reported on their GST / HST return in the reporting period it took place. Otherwise, it is reported by the end of the month following the purchase using form GST60.

The tax paid or self-assessed by the purchaser becomes the tax that is recoverable in the form of an Input tax credit (ITC) or a rebate.

How to File:

The election to file section 156 (1) must be made jointly by the qualifying group by completing form RC461 by the earliest date that a GST/HST return is due from the specified members who intend to make the election. Simply put, form RC461 is due on the earlier of the two corporations’ reporting period.

Conclusion

There are many pitfalls that may come into play when purchasing the assets of another corporation or partnership. Confusion may arise about whether GST/HST is applicable or exempt on a sale, which elections are relevant and whether conditions to qualify for an election have been satisfied. Where errors are made, there is the risk of not fulfilling one’s tax obligations to the CRA. It is always advisable to consult a tax or corporate lawyer to guide you through your transactions successfully.

FAQ’s:

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law Firm 2021