What to Consider when Buying or Selling a Business – Part I

What Considerations for Buying or Selling a Business Must I keep in Mind?

Looking to purchase a new business or sell your existing business? Sounds simple? Not always. There are vast considerations that must be contemplated and then negotiated in respect of buying or selling a business. In Part I of this Article, we discuss the most important consideration in the purchase or sale of a business which is whether the acquiring purchaser is to purchase the assets or the shares of the business. Both tax implications and liability concerns are associated with each type of sale.

A Seller Should Sell Shares

1. Tax Advantage – Capital Gains Exemption on Proceeds of Sale of Shares

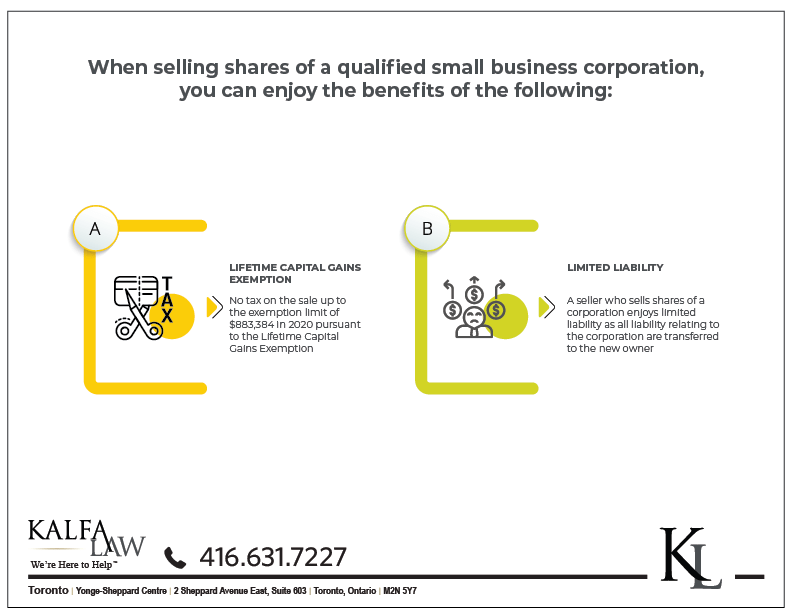

From a tax perspective, it is far more beneficial for a seller to sell its shares of a small business. This is because if the vendor corporation is a Canadian Controlled Private Corporation (CCPC) of which over 90% of its income is attributed to Active Business Income (ABI), the gain from the sale of the shares are exempt from taxation pursuant to the Lifetime Capital Gains Exemption (LCGE) of Qualified Small Business Shares (QSBC). The Lifetime Capital Gains Exemption allows each person an exemption of up to $866,912.00 on the sale of qualifying shares (in 2019).

How does the capital gains exemption work? It means that if you sell shares of a qualifying business for say $600,000, you will pay no tax on this income. You will pay no tax on any sale of shares under the exemption limit of $866,912.00. Where you sell shares for more than the correct exemption limit, you will only pay tax on the difference between your sale price and the $866,912 exemption.

The Lifetime Capital Gains Exemption is the only other type of capital gains exemption available to taxpayers in Canada, next to the Principal Residence Exemption for the proceeds of sale of one’s home in which they lived.

Few people know about the LCGE which happens to be an excellent tax planning and tax saving tool. For more information on the Lifetime Capital Gains Exemption, and whether your corporation will qualify, see our article What is the Lifetime Capital Gains Exemption?

2. Corporate Law Advantage – Limited Liability

A seller desires to sell its shares of a business for corporate law reasons too. Shares of a private corporation that has been active in the marketplace are saddled with liability. As long as the Seller holds onto the shares, his or her liability will continue to exist and accrue. By selling the shares of a corporation, the seller effectively transfers all of its liability too. The seller can easily walk away from the business and be secure that an old liability wont rear its ugly head months or even years later.

A Purchaser Should Purchase Assets

Of course, a purchaser wants something different. A purchaser typically wants to purchase the assets of a business, and not the shares. Quite simply, the purchaser doesn’t want to assume the liability of the entire corporation and all of its history in the marketplace.

A buyer is only interested in the business, not the business-vehicle that housed the business. A business can exist in any type of business vehicle (a sole proprietorship, a partnership or a corporation). A buyer wishes to procure the business from its business vehicle and dump it into a new business vehicle which belongs to the purchaser. This is called an asset purchaser or asset transfer.

An asset transfer occurs where all of the assets of a business are stripped from a corporation and transferred to the purchaser. The buyer then takes the assets and dumps them into a new sole proprietorship, partnership or corporation. The assets of a business are usually the physical assets, inventory, equipment, fixtures, products and intellectual property such as its name, website, trade-marks, trade-names, client lists, and goodwill in the marketplace.

Quite simply, the buyer wants the inventory, assets and goodwill of a business, not the liability of the corporation that operated the business using those assets.

Rules Can be Broken

However, every deal is different. Sometimes a buyer doesn’t want to purchase the assets, because the Undepreciated Capital Cost of the assets (carryforward of the depreciation) is nearly NIL. This eliminates a substantial deduction for the business, which will essentially increase the business’s taxable income. Instead, in this circumstance, the purchaser will prefer the shares of the business because they hope the business to grow and one day enjoy the LCGE exemption of $866,912 on its sale.

Also, a seller may not want to sell the assets of the business because if the assets are sold over and above the Undepreciated Capital Cost (UCC), recapture comes to play. Recapture is a tax penalty that occurs wherever assets are sold for more than its UCC. The CRA will levy tax on the difference in value between the business’s most recent UCC in its corporate return and the value of the sale. That is, if the business indicates a machine’s UCC to be $30,000, the business will be subject to a recapture tax if the machine is sold for $50,000.

Other Considerations

There are far more considerations to address other than whether the purchaser will purchase the assets or the shares of the business. Other important ticket items are the issue of employees and that of a non-competition agreement. These will be discussed in Part II – What to Consider when Purchasing or Selling a Business

Why You Need a Commercial Lawyer for Buying or Selling a Business:

The purchase and sale of businesses represents the crux of our firm, handling several transactions each month. With our combined tax and corporate law experience, we anticipate these complex corporate and tax issues and formulate optimal solutions that forward your interests. With years of experience in all issues of the purchase or sale of a business, we ensure that your interests are protected, you get the highest valuation for your business and pay the least tax.

For more information on our purchase and sale services, Contact Us today.

F.A.Q’s:

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law 2020

The above provides information of a general nature only. This does not constitute legal advice. All transactions or circumstances vary, and specified legal advice is required to meet your particular needs. If you have a legal question you should consult with a lawyer.