Tax elections on the sale of a business: Avoiding GST/HST with the filing of Election 167

When selling a business in Canada, many buyers and sellers are surprised to learn that GST/HST may be payable in addition to the purchase price. Unless a tax election applies, the purchaser must pay GST/HST on the sale, and the vendor is responsible for collecting and remitting it to the Canada Revenue Agency (CRA).

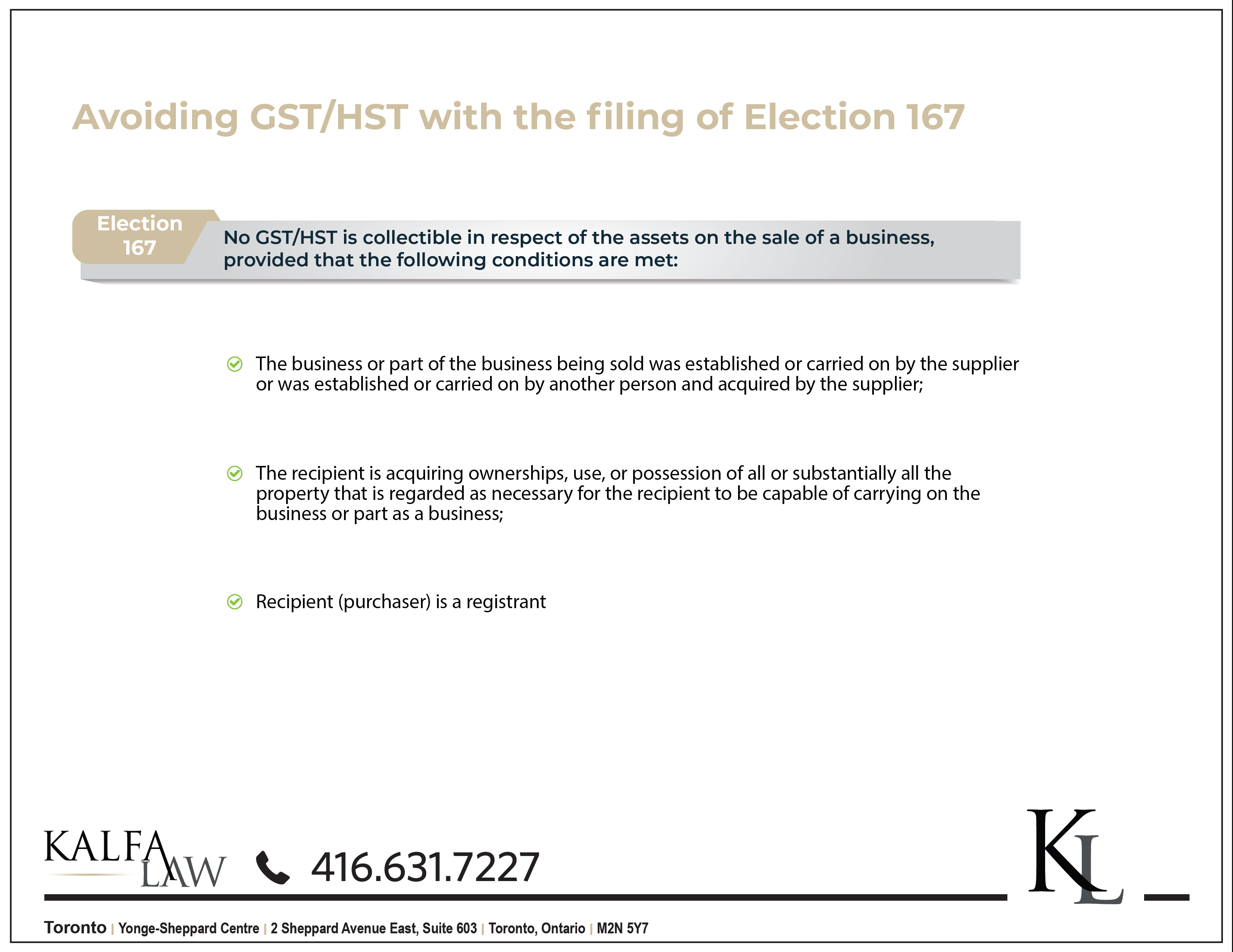

However, if the parties file a joint election under Section 167 of the Excise Tax Act (ETA), the business may be transferred with no GST/HST payable, provided certain conditions are met.

This election exists because, in most cases, the purchaser would otherwise pay GST/HST and then immediately claim it back as an input tax credit—making the transaction a wash for CRA. The election removes this unnecessary administrative step.

Below, we break down what Election 167 is, who qualifies, exceptions, when to file, and how to submit the election.

What Is Section 167 of the Excise Tax Act?

Section 167 of the ETA governs two possible GST/HST elections:

- 167(1) – Applies to the sale of a business or part of a business.

- 167(2) – Applies to the sale of business assets of a deceased individual.

This article focuses on subsection 167(1), which applies to the sale of an operating business.

The key question determining eligibility is:

Are the assets being sold substantial enough that the purchaser can carry on the business after the sale?

If the answer is yes—and other conditions are satisfied—GST/HST may not apply.

Conditions Required for Election 167(1)

To qualify, all of the following must be true:

1. A Business (or Part of a Business) Is Being Sold

The supplier must be selling a business that:

- It operated, or

- It acquired from another party.

2. The Purchaser Must Acquire “All or Substantially All” Business Assets

The buyer must receive 90% or more of the property necessary to run the business, which may include:

- Tangible assets – equipment, vehicles, furniture

- Intangible assets – goodwill, trademarks, business name

- Capital real property – land, buildings

This requirement ensures the business can continue operating immediately after closing.

3. The Purchaser Must Be GST/HST Registered

Contrary to popular belief, only the purchaser must be registered for GST/HST. The vendor does not need to be registered, although most business vendors typically are if their revenue exceeds $30,000 annually.

Real-World Example of Election 167

Qualifying Example

A purchaser buys a pizza business including:

- Building and parking lot

- Kitchen equipment

- Delivery vehicles

- Office equipment

- Goodwill and business name

Even if the buyer must purchase new chairs and tables after closing, the total acquisition still exceeds 90% of the assets required to operate. Therefore the transaction qualifies for Election 167 and may avoid GST/HST.

Non-Qualifying Example

If the purchaser only buys:

- The oven, and

- Office equipment

This is not the sale of a business—it is simply the sale of assets. In this situation, election 167 does not apply, and GST/HST must be charged.

Exceptions – When Election 167 Cannot Be Used

Even if most conditions are met, the election cannot be applied in certain cases, including:

1. The Assets Are Leased or Licensed

If property is not sold, but leased or licensed, then GST/HST applies as usual.

2. The Vendor Continues to Provide Services

If the seller continues offering services after the sale, those services remain taxable.

3. The Business Deals in Exempt Supplies

Businesses that operate primarily in exempt supplies under Schedule VI of the ETA (e.g., certain financial services) cannot make the election.

4. Zero-Rated Goods Still Qualify

Goods taxed at 0% (due to “place of supply” rules) do not prevent the election, and can still fall under Section 167.

When Must Election 167 Be Filed?

The purchaser is responsible for filing the GST44 election form ‘on or before the day the purchaser would otherwise have been required to file a GST/HST return for the period in which tax would have been payable.’

In simple terms, file the election before the end of the purchaser’s reporting period, whether monthly, quarterly, or annually.

Even though the buyer files the election, the seller has a vested interest in ensuring it is submitted—otherwise, the seller may still be liable for GST/HST they did not collect.

How to File the GST/HST Election Under 167(1)

Filing Steps

- Vendor and purchaser complete GST44 (Election Concerning the Acquisition of a Business).

- The buyer files the form with the CRA, either:

- Electronically through their tax preparer, or

- By submitting it to their local tax centre.

- The form must be filed with the GST/HST return for the reporting period in which the acquisition occurred.

Since reporting periods vary by business (monthly, quarterly, or annual), professional advice is recommended to avoid late filing.

Conclusion

If you are buying or selling a business, understanding Section 167 of the Excise Tax Act can prevent unnecessary GST/HST costs and compliance issues. When used correctly, Election 167:

- Allows qualifying business sales to proceed without GST/HST, and

- Eliminates the need for the purchaser to claim back tax through input tax credits later.

To ensure you qualify and file correctly, contact a lawyer at Kalfa Law Firm for assistance with business purchase and sale transactions.

FAQs:

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law Firm 2025