Should Your Business be run as a Sole Proprietorship?

A sole proprietorship is the most basic form of business organization that occurs when one person, acting alone, pursues a business endeavour with a view for profit. While a sole proprietorship is not a corporation, it nevertheless must be assigned a Business Number (BN) from the CRA. Sole proprietors file their business taxes together with their personal T1 tax return by completing an additional scheduled called a form T2125.

A sole proprietorship arises the moment you sell goods or services. If you operate under your legal name (i.e. Sally Smith), no registration is needed. Sole proprietors need to register with the Provincial Ministry only if they operate a business under a trade name other than their own legal name (i.e. Sally’s Sunshine Landscaping), while registration with the CRA is necessary only if sales exceed $30,000 a year.

The advantages of running a business as a sole proprietorship basically relate to the simplicity of setting it up and maintaining it as well as the simplified tax structure. Let’s look at these in greater detail.

Simple to Set Up and Maintain

Setting up as a sole proprietorship is simple and inexpensive to set up. The regulatory burden is light with minimal paperwork and legal costs. Moreover, there are no employees, partners, or investors to contend with, which may be advantageous if your business earns less than $100,000 a year. The simplicity of the sole proprietorship makes a great deal of sense, particularly if don’t envision selling your business or passing on your business to heirs.

Simplified Tax Structure

A sole proprietorship is a pass-through tax entity. A pass-through entity is a special business structure that is used to reduce the effects of double taxation. That means that there is no tax paid at the sole proprietorship level. Instead, all profits flow to the sole proprietor directly.

While this simplified structure avoids double taxation, the tax rate on profits from sole proprietorship’s are higher than other business structures, such as a corporation. Moreover, a sole proprietor cannot take advantage of certain tax saving tools, such as the Lifetime Capital Gains Exemption or income splitting with family members. It is also important to keep in mind that a sole proprietor is personally liable for a business’s debt, and, it is therefore advisable that he/she take out a personal liability insurance policy.

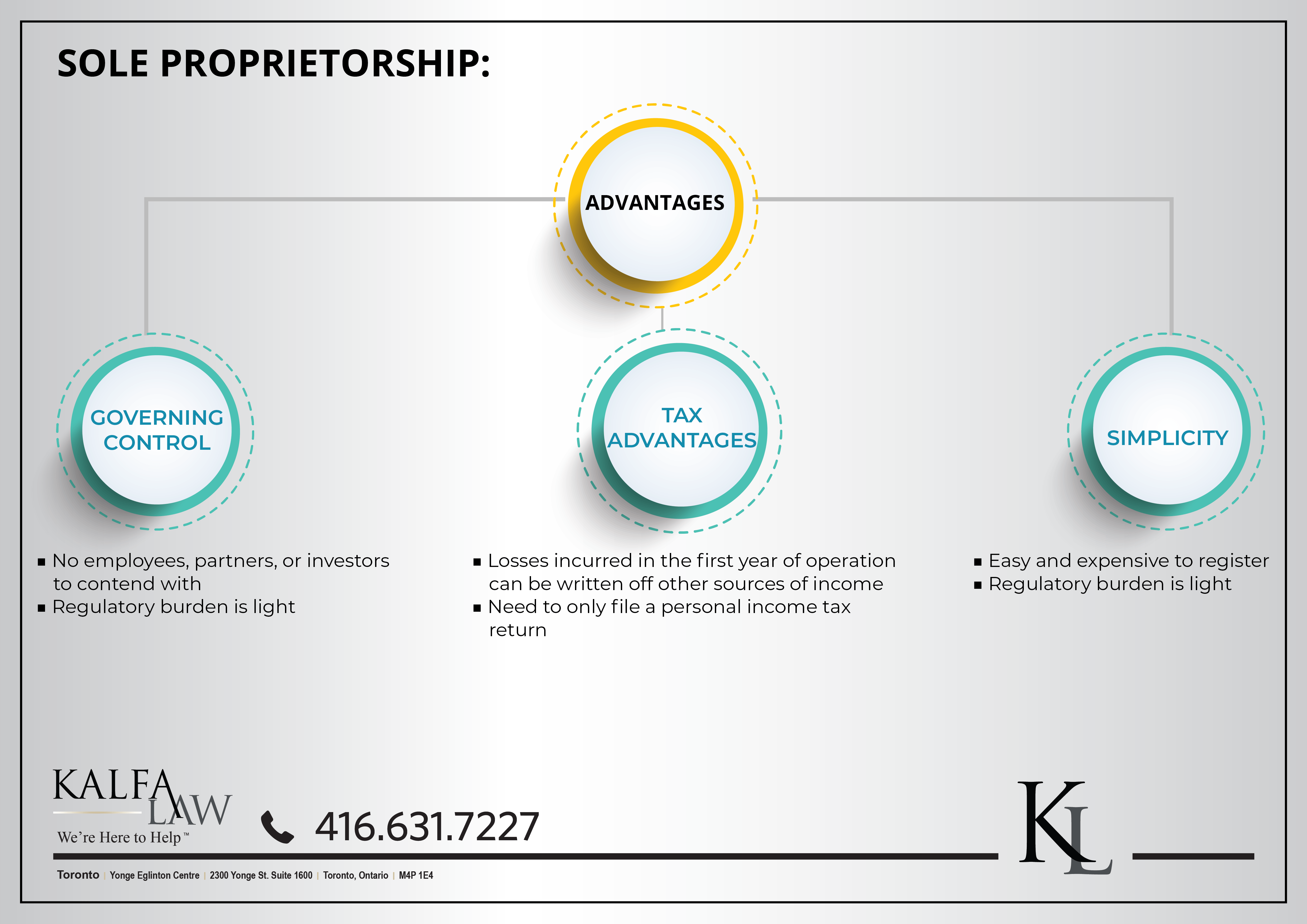

Advantages of Sole Proprietorship:

• Easy and inexpensive to register.

• Regulatory burden is generally light.

• You have direct control of decision making.

• Minimal working capital required for start-up.

• Some tax advantages if your business is not doing well.

• All profits go to you directly.

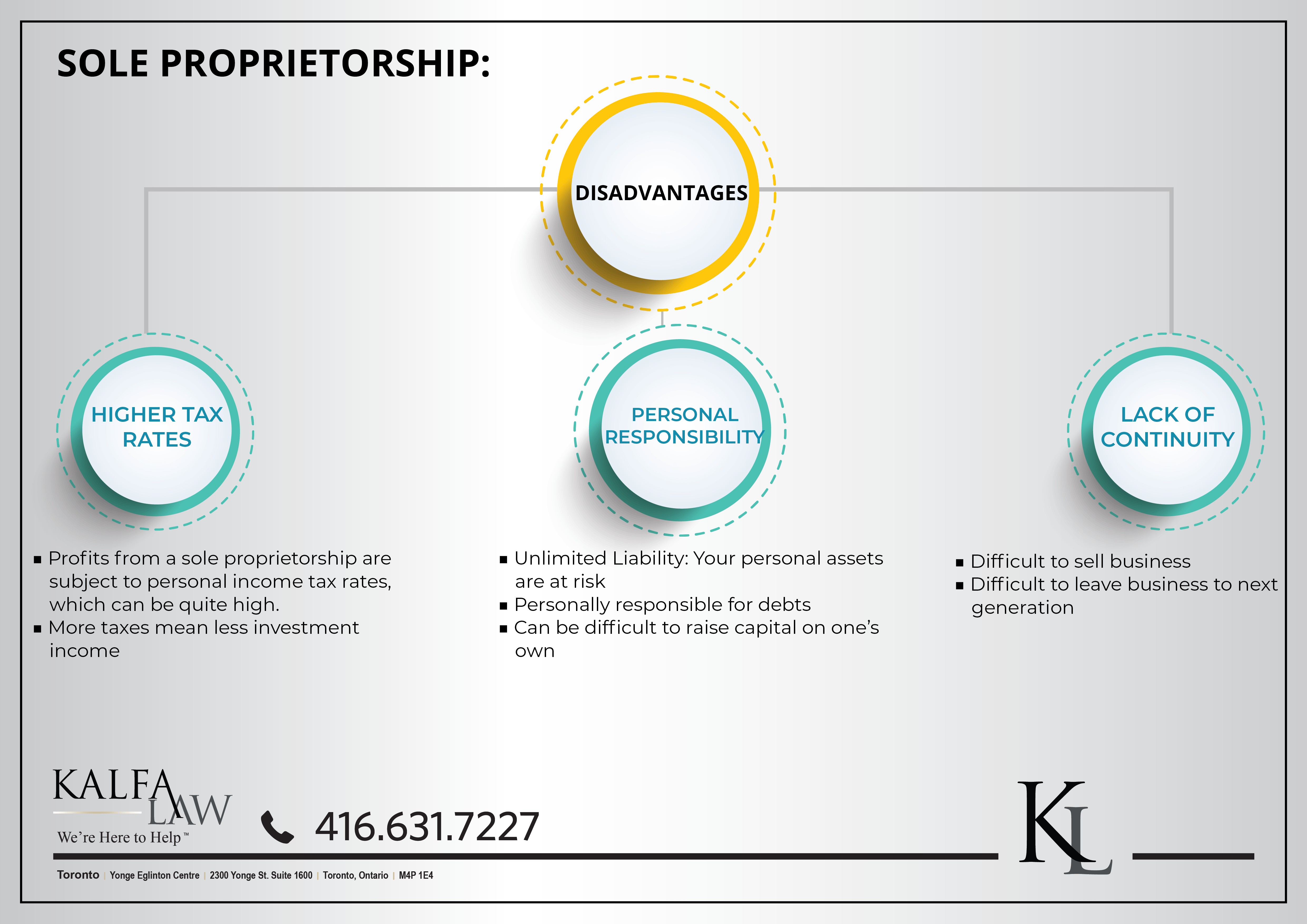

Summary of Disadvantages of Sole Proprietorship:

• Unlimited personal liability. Your personal assets are at risk.

• Income is taxable at your personal rate and, if your business is profitable, this could put you in a higher tax bracket.

• Pay tax on all of the business income you earn at a high tax rate; lose investment income.

• Lack of continuity for your business if you are unavailable; difficulty of transitioning business to next generation or selling business.

• Can be difficult to raise capital on your own.

F.A.Q’s:

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law Firm 2020

The above provides information of a general nature only. This does not constitute legal advice. All transactions or circumstances vary, and specified legal advice is required to meet your particular needs. If you have a legal question you should consult with a lawyer.