Essentials of the Business Loan Agreement

A business loan agreement is an agreement between a lender and a borrower, whereby the lender promises to loan money and the borrower promises to pay it back. To ensure that the borrower holds to its end of the bargain, the corporation typically must provide security and collateral to ensure that the loan is repaid.

The Lender is the person or corporation that loans something of value (money, property or some service) to the Borrower on condition that the Lender will be paid a certain amount in the future.

The Borrower is the person or corporation that receives value (money, property or some service) from the Lender on the condition that the Borrower will pay the principal amount plus any interest to the Lender at some time in the future.

The business loan agreement is a contract that is often required under a variety of circumstances, such as starting a business, buying a building, buying equipment, or buying products to build an inventory to sell. It specifies the amount of the loan, the rate of interest, terms of repayment, and payment dates so that both the borrower and lender have a clear outline of the terms of the loan.

The Elements of a Business Loan Agreement

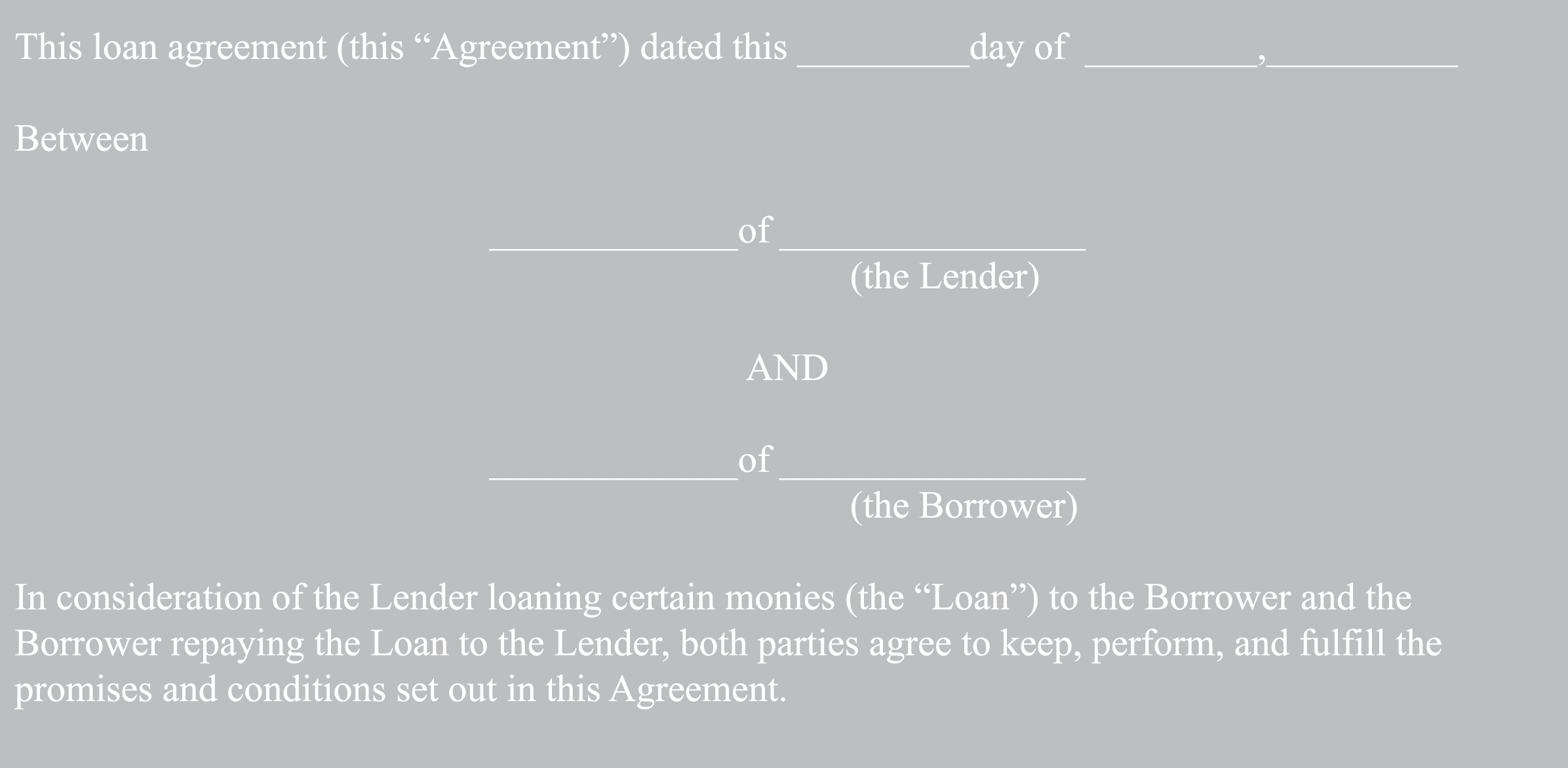

1. The Opening:

A loan agreement begins with the names and residential locations of the two parties—lender and borrower—who enter in the business agreement, along with the general obligations of each party to the other and the date on which the loan monies will be disbursed to the borrower.

If there is a cosigner or guarantor who is assisting the borrower by providing a down payment, putting up collateral or a personal guarantee, this person is also described in this section.

The language will typically look like this:

2. The Loan Amount and Interest:

A lender must tell you the annual percentage rate (APR) before you sign a loan agreement. To understand the APR of a loan, make sure you ask:

How much total interest will I pay?

Are there any fees or extra charges?

Are there any other costs, including loan insurance? (For example, with a mortgage loan, you must get mortgage insurance if your down payment is less than 20 percent of the principal.)

The lender should also indicate the method used to calculate the cost of borrowing. For example, with mortgages and other loans, lenders use the remaining balance method. They multiply the interest rate by the principal balance at the start of the term. Each payment includes some of the principal amount. You don’t pay interest on any principal you have repaid.

3. The Date the Payment is Due:

4. Defaults and Penalties:

Both parties have made promises, and if one party doesn’t fulfill its promises, the agreement is in default. If the borrower defaults on the loan (doesn’t meet the terms and conditions), the loan agreement spells out any fines and penalties. Each month, there is usually a grace period, which is a certain number of days after the due date when the loan can be paid without penalty. If the payment isn’t made within the grace period, the agreement spells out penalties.

There also may be an acceleration clause, which indicates that the loan is immediately due and payable.

5. Governing Law:

Business loans are subject to provincial laws, which differ from province to province. Your loan agreement should include a sentence about which state law governs.

6. Costs:

The borrower will be asked to make representations regarding his obligations as the borrower, ensuring the collateral assets are in good standing, as well as costs associated with lawyer fees and collection fees if the loan goes into default.

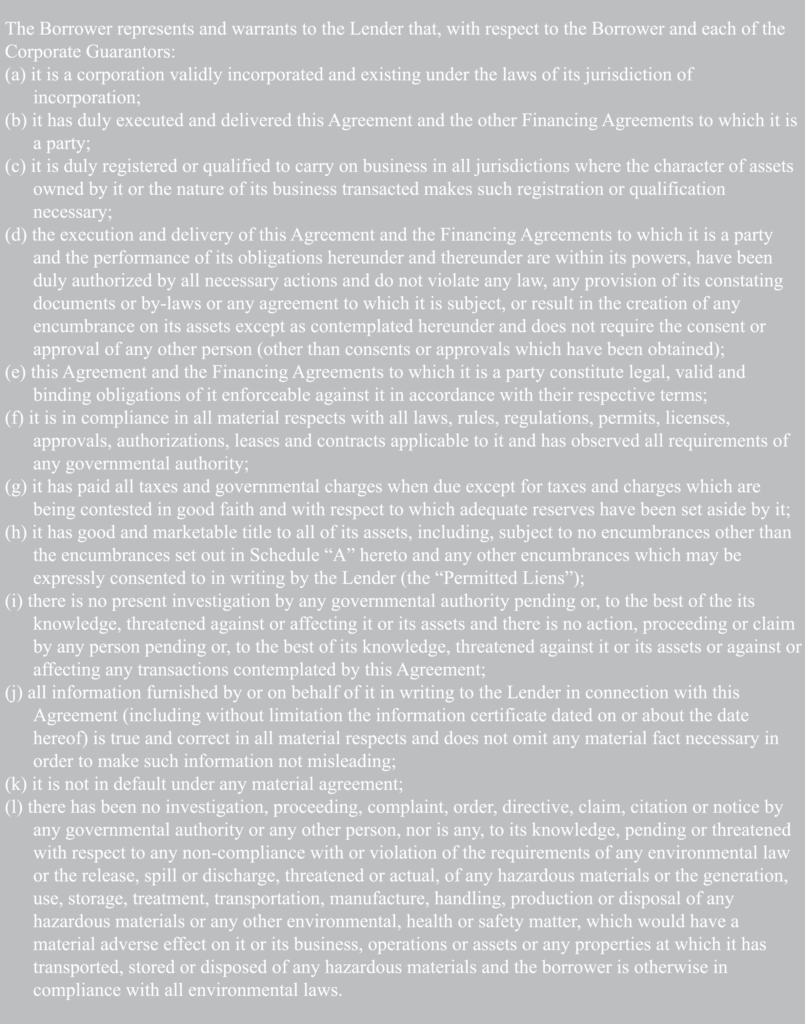

7. Representations of the Borrower:

The borrower will be asked to affirm that certain statements are true with respect to the viability of his business and ability to repay the loan. Among the most common representations to which the borrower must attest, are the following assurances:

- Your assurance that you are legally able to do business in the province.

- Your assurance that you have filed all your tax returns and paid all of your taxes

- Your assurance that there are no liens or lawsuits against the business that could affect its ability to pay back the loan

- Your assurance that the financial statements of the business are true and accurate.

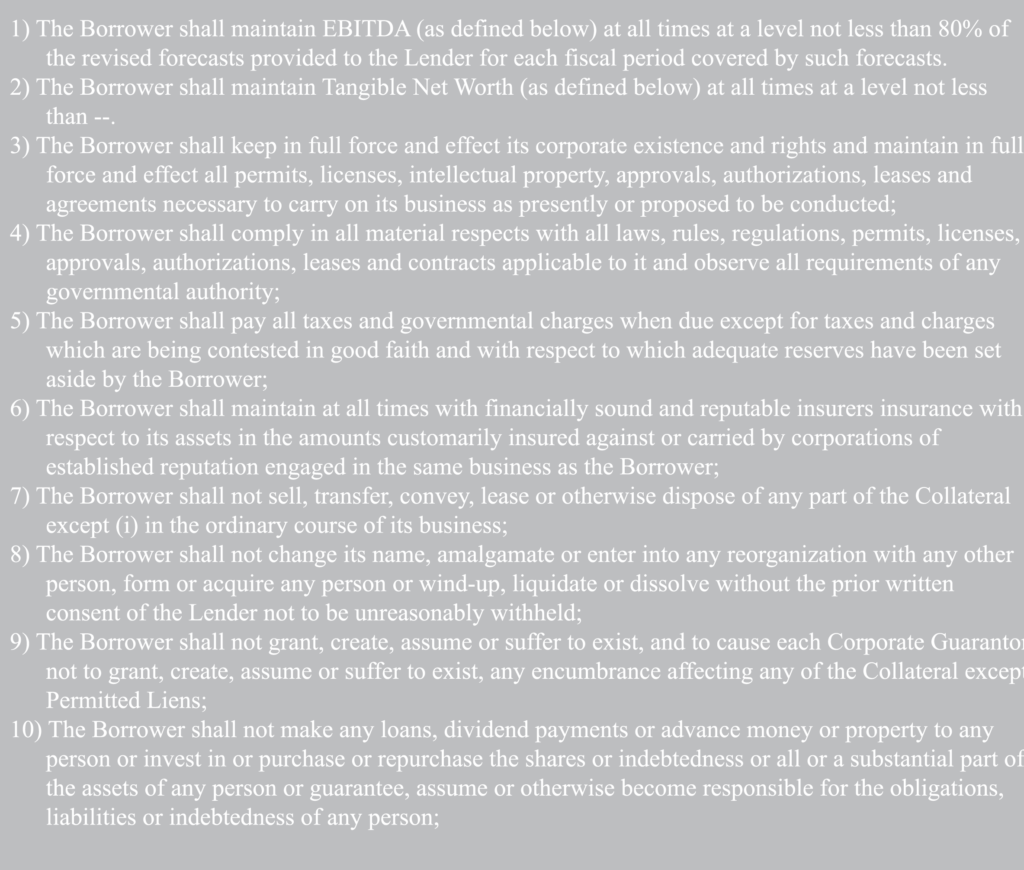

8. Covenants:

Covenants are promises made by both parties. Most lenders will require several covenants as part of the loan agreement:

- Proof of insurance: or whatever other security or collateral you will be using to ensure that the lender is paid at least a part of the loan in case of default.

- Life Insurance: many business loans require the borrower to take out life insurance in case something happens to him with the lender as the beneficiary.

- Guarantees that the business will not take on additional debt or that management will not change.

- For larger loans, particularly for startups, many lenders require periodic financial statements showing that the business will continue to be able to pay back the loan.

9. Binding Effect

The agreement will usually include a clause so that the agreement remains valid, binding, and enforceable should the borrower die or become unable to repay the loan. This clause will reference the borrower’s ”heirs, successors, and assigns” to ensure that the loan continues to be repaid.

10. Amendments

A clause that references how the loan agreement can be amended or modified in the future.

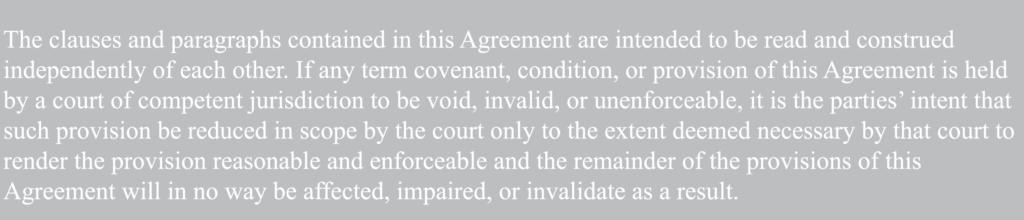

11. Severability

Severability, also known by the Latin term “salvatorius,” is a provision in a piece of legislation or a contract that allows the remainder of the legislation’s or contract’s terms to remain effective, even if one or more of its other terms or provisions are found to be unenforceable or illegal.

The agreement ends with a statement regarding general provisions related to the use of language and a summary statement indicating that there are no further provisions or items, oral or otherwise to be included. Following these, the agreement is signed by a witness and by the Borrower and the Lender, with the date and year included.

While you may be tempted to use a free template online, be wary as every business loan agreement is unique and all terms are negotiable. It is advisable to have a business loan agreement lawyer review the agreement to ensure that all specific covenants and guarantees are included that will protect you. Contact a business loan agreement lawyer at Kalfa Law Firm to help you draft a business loan agreement that is viable and enforceable.

You work hard for your money. We work hard for you to keep it ™ .

FAQ’s:

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law 2020

The above provides information of a general nature only. This does not constitute legal advice. All transactions or circumstances vary, and specified legal advice is required to meet your particular needs. If you have a legal question you should consult with a lawyer.