The Difference Between An Employee and Independent Contractor

Are you an employee and an independent contractor? What is the difference, what are the tax advantages of each and how does the CRA make the assessment in determining what your status is?

Whether you are starting up a new business or manage an existing business, it is important to understand the distinctions between an employee and an independent contractor at law. At the start of a business relationship, a worker and business often set up their relationship as an independent contractor which provides the business with the advantage of not having to deduct and remit source deductions of EI, CPP, and income taxes nor pay workplace safety insurance premiums.

It also permits the worker to be able to deduct business expenses from his or her income. Sounds good to all parties. Be careful though, mischaracterizing an employer-employee relationship to avoid taxes and source deductions may run afoul of the law and result in serious penalties.

Even if both the business and the worker consider the relationship to be one of contract, this does not mean the Canada Revenue Agency (CRA) will agree. The Canada Revenue Agency (“CRA”) may audit the business and determine that the relationship is actually one of employment. In that case, they will demand the employer remit all past unremitted EI and CPP, together with penalty charges and interest.

Further, the employer’s directors may be held personally liable for the failure to remit the source deductions. On the employee side, he or she may be assessed for unremitted income tax and past claimed business expenses may be disallowed resulting in a massive tax bill.

In order to avoid an aggressive audit, it is important to understand how the CRA distinguishes between an employee and an independent contractor at law, and ensure that employees are properly paid as such.

CRA – The Two Part Test

The central and overarching question the CRA asks in determining the distinction between an employee and an independent contractor is whether the person is engaged to carry out services as a person in business on his own account, or as an employee. In order to get down to the crux of this issue, the CRA engages a two part test.

- Intent of the Parties

The CRA will first look to the intent of the parties when the relationship was formed. Did the two parties intend to enter into a contract of service (employer-employee relationship) or did they intend to enter into a contract for services (business relationship)?

A written agreement can help create clarity as regards the intent of the relationship and is therefore highly recommended. However be cautioned that an independent contractor’s agreement is not categorically determinative; notwithstanding a well drafted agreement, there remains the chance that the CRA will determine that the true nature of the relationship was that of an employee and impose the aforementioned costs and penalties.

- True Nature of Relationship

The test that the CRA uses to determine the true nature of the relationship is often regarded as the ‘control’ test. It has 4 clear aspects:

- Does the worker have control over where and how he or she works;

- Can the worker hire assistants or sub-contract work;

- Does the worker provide his or her own equipment and tools; and

- Has the worker taken a financial risk and has the opportunity to profit from his or her work;

Factors to Consider – A Closer Look

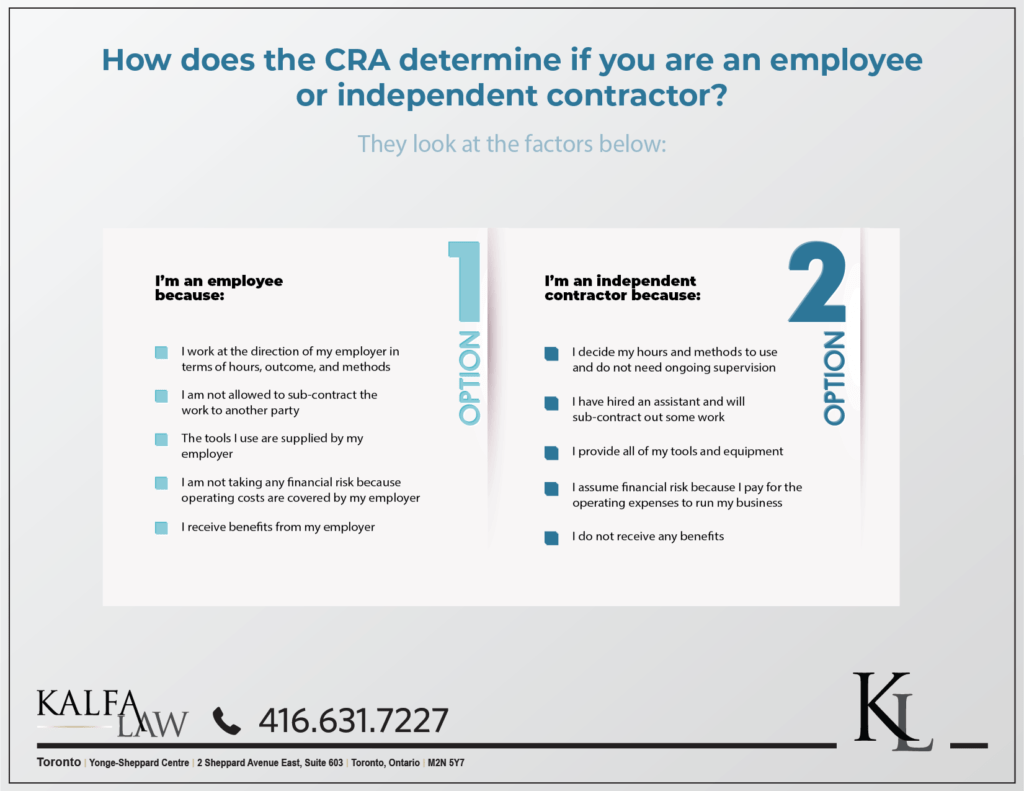

1) Control

Control is the ability, authority, or right of a payer to exercise control over a worker concerning the manner in which the work is done and what work will be done.

Factors indicating a worker is an employee

- The relationship is one of subordination. The payer will often direct, scrutinize, and effectively control many elements of how and when the work is carried out.

- The payer controls the worker with respect to both the results of the work and the method used to do the work.

- The payer chooses and controls the method and amount of pay. Salary negotiations may still take place in an employer-employee relationship.

- The payer decides what jobs the worker will do.

- The payer chooses to listen to the worker’s suggestions but has the final word.

- The worker requires permission to work for other payers while working for this payer.

- Where the schedule is irregular, priority on the worker’s time is an indication of control over the worker.

- The worker receives training or direction from the payer on how to do the work. The overall work environment between the worker and the payer is one of subordination.

Factors indicating that a worker is an independent contractor

- A self-employed individual usually works independently.

- The worker does not have anyone overseeing his or her activities.

- The worker is usually free to work when and for whom he or she chooses and may provide his or her services to different payers at the same time.

- The worker can accept or refuse work from the payer.

- The working relationship between the payer and the worker does not present a degree of continuity, loyalty, security, subordination, or integration, all of which are generally associated with an employer-employee relationship.

2) Subcontracting work or hiring assistants

Consider if the worker can subcontract work or hire assistants. This factor can help decide a worker’s business presence because subcontracting work or hiring assistants can affect their chance of profit and risk of loss.

Factors indicating a worker is an employee

- The worker cannot hire helpers or assistants.

- The worker does not have the ability to hire and send replacements. The worker has to do the work personally.

Factors indicating that a worker is an independent contractor

- The worker does not have to carry out the services personally. He or she can hire another party to either do the work or help do the work, and pays the costs for doing so.

- The payer has no say in whom the worker hires.

3) Tools and equipment

Consider if the worker owns and provides tools and equipment to accomplish the work. Tools and equipment can vary widely in terms of value and can include everything from wrenches and hammers, to specialized clothing, appliances, stethoscopes, musical instruments, computers, and vehicles such as trucks and tractors.

Self-employed individuals often supply the tools and equipment required for a contract. As a result, the ownership of tools and equipment by a worker is more commonly associated with an independent contractor’s relationship.

However, employees sometimes also have to provide their own tools. The courts have acknowledged that because a worker is required to provide tools of the trade, this does not in itself mean that the worker is a self-employed individual. For example, many skilled tradespeople such as auto mechanics have to supply their own tools, even if they are full-time employees.

Factors indicating a worker is an employee

- The payer supplies most of the tools and equipment the worker needs. In addition, the payer is responsible for repair, maintenance, and insurance costs.

- The payer retains the right of use over the tools and equipment provided to the worker.

- The worker supplies the tools and equipment and the payer reimburses the worker for their use.

Factors indicating that a worker is an independent contractor

- The worker provides the tools and equipment needed for the work. In addition, the worker is responsible for the costs of repairs, insurance, and maintenance to the tools and equipment.

- The worker has made a significant investment in the tools and equipment and the worker retains the right over the use of these assets.

- The worker supplies his or her own workspace, is responsible for the costs to maintain it, and does substantial work from that site.

4) Financial risk and chance of profit

Consider the degree of financial risk taken by the worker. Consider if there are any fixed ongoing costs incurred by the worker or any expenses that are not reimbursed. Usually, employees will not have any financial risk as their expenses will be reimbursed, and they will not have fixed ongoing costs.

Self-employed individuals, on the other hand, can have financial risk and incur losses because they usually pay fixed monthly costs even if work is not currently being done.

Employees and self-employed individuals may be reimbursed for business or travel expenses. Consider only the expenses that are not reimbursed by the payer.

Consider also whether the worker can realize a profit or incur a loss, as this indicates that a worker controls the business aspects of services rendered and that an independent contractor relationship likely exists. To have a chance of a profit and a risk of a loss, a worker has to have potential proceeds and expenses, and one could exceed the other.

Factors indicating a worker is an employee

- The worker is not usually responsible for any operating expenses.

- Generally, the working relationship between the worker and the payer is continuous.

- The worker is not financially liable if he or she does not fulfil the obligations of the contract.

- The payer chooses and controls the method and amount of pay.

Factors indicating that a worker is an independent contractor

- The worker hires helpers to assist in the work. The worker pays the hired helpers.

- The worker does a substantial amount of work from his or her own workspace and incurs expenses relating to the operation of that workspace.

- The worker is hired for a specific job rather than an ongoing relationship.

- The worker is financially liable if he or she does not fulfil the obligations of the contract.

- The worker does not receive any protection or benefits from the payer.

- The worker advertises and actively markets his or her services.

Employees – Advantages and Disadvantages

Employees have certain entitlements, such as CPP and EI benefits as well as protection under employment standards, health and safety and workers’ compensation laws. As an employee, an employer is required to deduct CPP and EI, also known as source deductions, from the employees payroll and remit the funds to the Receiver General. Accordingly, the employee will qualify for employment insurance should he or she lose their job and will be eligible for the Canada Pension Plan at retirement.

An employee is also afforded the rights and privileges under the Employment Standards Act (“ESA”) which include vacation pay, statutory holiday pay, restrictions on the hours of work per day or per week, minimum wage, eating periods, pregnancy and parental leave, overtime pay and termination pay, among other advantages. The employer will also have to pay into the Workplace Safety and Insurance Board program (“WSIB”) which will allow the employee to gain compensation for an injury at work should one arise. All of these advantages accrue only to legal employees.

Some disadvantages is that an employee may be limited in the amount of business expenses he or she may deduct from their annual tax obligations, they pay into EI and CPP from their own wages and they have less control over the manner and hours in which they work.

Independent Contractors – Advantages and Disadvantages

Independent contractors (“IC”) on the other hand do not have to pay into employment insurance or CPP and the employer does not have to remit into WSIB. An independent contractor is not entitled to the benefits afforded under the Employment Standards Act such as vacation pay, termination pay and severance. An independent contractor will not be entitled to collect EI if he or she loses her job.

However on the upside, an independent contractor can deduct a whole host of business expenses from his or her gross income and thus pay tax on the net income as opposed to its gross income. An independent contractor is also not subject to EI or CPP deductions. An independent contractor does not have to pay tax on his income every pay period as an employee does. In this way, it can invest the funds in a higher interest vehicle and pay its tax liability once a year. This tax deferral provides a great tax planning tooling that employees are not afforded.

Be Careful – Choose Wisely

For the reasons above, most individuals want to be characterized as independent contractors and not employees. Be wary however. Just because both parties agree that this will be the arrangement, does not mean that it is (a) legal and (b) that it will pass muster with the CRA. Intention of the parties is only one aspect of the test, and a very small part of the overall assessment. If the nature of the employment appears to be that of an employee, based on the factors assessed above, be sure to be paid accordingly in order to avoid harsh penalties and interest at the hands of the CRA for mischaracterizing the employment in order to gain an unfair tax advantage.

FAQ’s:

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

The above provides information of a general nature only. This does not constitute legal advice. All transactions or circumstances vary, and specified legal advice is required to meet your particular needs. If you have a legal question you should consult with a lawyer.