Allocations of Purchase Price on the Sale of a Business – Be Wary of Section 68

When buying or selling the assets of a business, it is important to negotiate how the purchase price is allocated, as there are significant tax consequences on both the seller and purchaser depending on how the allocation is made. In making an allocation, the proceeds of the sale must be explained as being allocated to either inventory; depreciable capital (property resulting in a capital gain upon its disposition); eligible capital property, such as goodwill, licenses, franchises, concessions; or non-depreciable capital property, such as land or partnership interests, which increase in value over time.

The allocation of the purchase price determines the vendor’s income tax that results from the sale, as well as the purchaser’s sales taxes on the purchase price. Furthermore, how the purchase is allocated will determine the purchaser’s future tax savings from the amortization of the cost of the assets for purposes of using the depreciated value of the assets as a tax deduction.

Generally speaking, wherever there is a tax advantage on one party there is a concomitant tax disadvantage on the other party and vice versa. An allocation that results in the little tax to the vendor generally results in costs that are not deductible or are deductible only over a period of time to the purchaser.

Let’s look more closely at how the allocation of the purchase price when buying or selling the assets of a business will impact the tax obligations on both the vendor and purchaser.

Vendor’s Allocation: Tax Implications

Non-Depreciable Capital Property

It is no surprise that the Vendor is usually concerned with achieving whatever allocation results in the least tax. As such, the vendor is inclined to allocate the proceeds of disposition to non-depreciable capital property such as land or partnership interests, as only 50% of the realized gain is included in income.

Inventory and Depreciable Capital Property

In contrast to the tax advantages for the vendor on the sale of non-depreciable capital property, proceeds from inventory is deemed as income and fully taxable. With regards to depreciable capital property, which includes goodwill as of the new rules effective January 2017, any proceeds in excess of UCC (undepreciated capital cost) will be fully included in the seller’s income via the ITA’s recapture tax.

Conversely, if the amount allocated to depreciable capital assets is less than the UCC, the seller will be able to deduct this amount as a loss from their income for the year in which the transaction is made.

Purchaser’s Allocation

Non-depreciable capital property

As opposed to the tax advantage for the vendor when selling non-depreciable capital property, there accrues a tax liability on these assets for the purchaser, as there are no ongoing deductions available to reduce the income of the purchaser. Moreover, the transfer of some non-depreciable capital property, such as land, is subject to additional taxes (i.e., the land transfer tax).

Inventory and Depreciable Capital Property

A purchaser will generally prefer to allocate as much of the purchase price as possible to inventory as the purchaser’s cost of inventory is deducted from the revenue received when the inventory is sold.

As for depreciable capital property, the purchaser is entitled to deduct a portion of the total cost of each class of depreciable property each year that it is held as income on a declining-balance basis.

Opposing Interests

Given the opposing interests in terms of asset allocation on the sale of a business for the vendor and purchaser, the CRA usually accepts a mutually agreeable allocation as long as it appears that there has been a bona fide negotiating process between the parties. A negotiating process between parties of different interests signals to the CRA that the monies in question have been made legitimately.

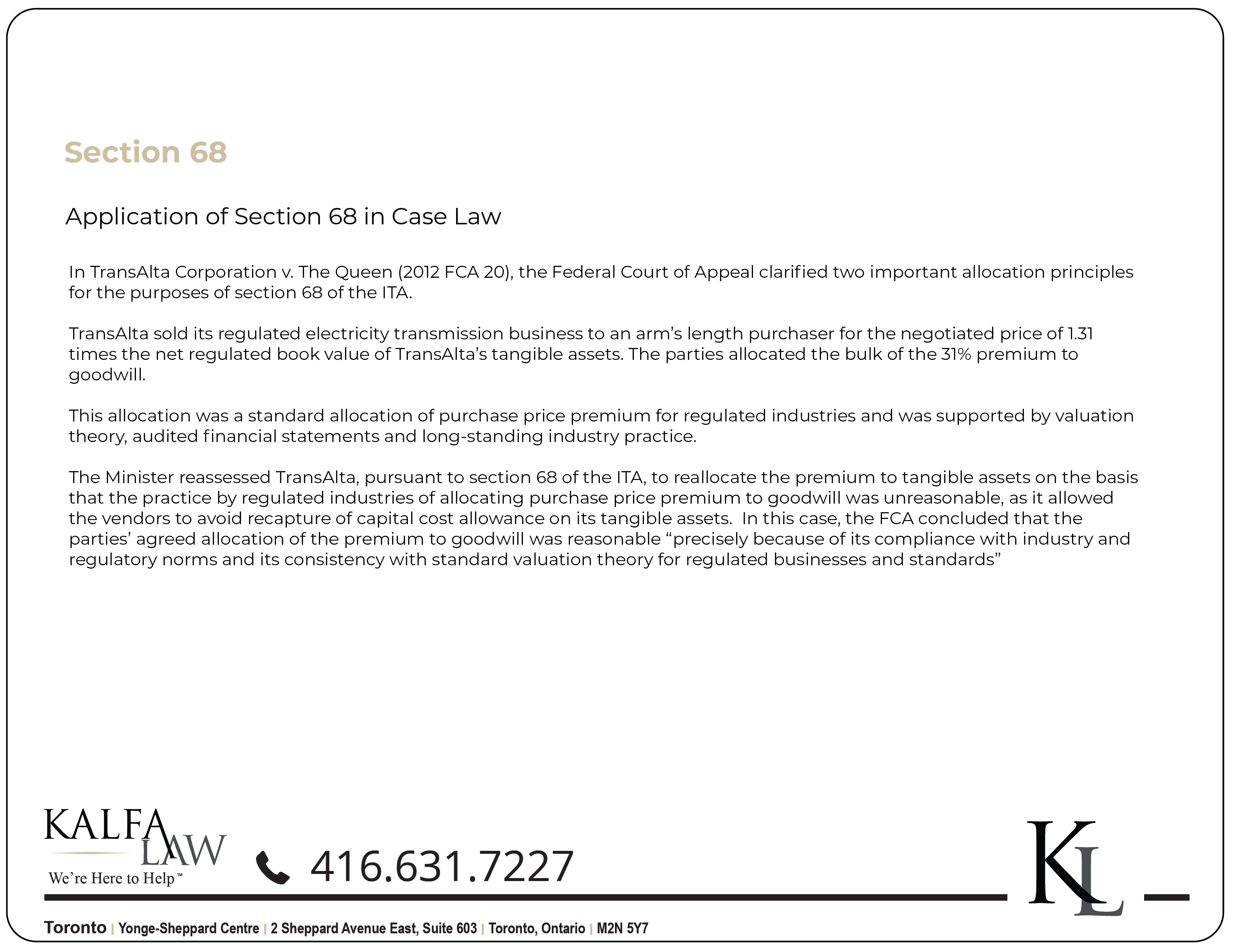

There are instances, however, where income credited to a party in the course of an asset sale transaction may appear suspicious. This is where section 68 of the ITA comes in. Section 68 gives the CRA the power to set aside allocation if bona fide arms-length negotiations for the allocation have not taken place. The Assessing Officer should accept the allocation of the purchase price when there has been hard bargaining and there is no apparent sham or subterfuge. Further, the reasonableness of the allocation must be considered from both the purchasers and the vendor’s perspective by the Assessing Officer.

Section 68 may apply in the following circumstances:

- the allocation of the purchase price is not reasonable in the circumstances; and

- there is no evidence of hard bargaining between the purchaser and the vendor about the allocation

Section 68 of the Income Tax Act allows the CRA to determine the reasonable consideration for the disposition of a particular property despite the allocation by the parties. In addition to the cash credits from the sale of assets, Section 68 has been significantly revised to encompass services as well as property. The inclusion of service affects situations in which amounts are paid to the vendor for services, especially consulting services or retiring allowances, concurrent with the purchase of the vendor’s assets.

Unexplained cash credits that are suspicious are taxed at a flat rate of 60% in addition to a surcharge of 25% and a penalty of 6%. The final tax rate comes to 83.25%. No deduction or allowance is allowed and no loss can be set off against such unexplained cash credit which is considered income.

Section 68 then is used in order to validate cash transactions between parties where there are red flags, such as the allocation of the purchase price is not reasonable or there is no evidence of hard bargaining between the purchaser and the vendor about the allocation. The section is most often used by the CRA to uncover any suspicious activity behind unexplained cash credits transferred by third parties who are interested in evading taxes.

However, it is entirely possible that legitimate transactions raise red flags, such as when one of the parties is indifferent to the allocation or when the purchaser and the vendor do not deal at arm’s-length.

Why would there be indifference? It is possible for a vendor to be indifferent when its carryovers would otherwise expire or there are sufficient cost amounts for the assets to prevent the creation of taxable income from the sale.

Even with legitimate reasons for indifference or the absence of bonafide negotiations between the parties, both the vendor and purchaser must be aware and vigilant against the reach of the CRA through section 68. The purchaser and the vendor should therefore agree on allocations and file their tax returns consistently. Consistency is the hallmark of hard bargaining and consensus on allocation.

Therefore, ensure that regardless of the tax result to the vendor or purchaser, bona fide negotiations in respect of allocation occur. These can easily be documented with solicitor emails.

Contact a lawyer at Kalfa Law Firm to help with determining how best to allocate the purchase price on the sale of your business’s assets so as not to trigger the use of section 68 by the CRA.

FAQ’s:

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law Firm 2021