All About Canadian Corporations

Canadian Corporations

A Canadian corporation is the most common form of business organization. It is a registered separate legal entity that can be operated by one or more persons. A corporation has its own tax obligations and must file its own income tax return called a T2 return. In spite of the rigorous governance, the corporation has several advantages, including various tax benefits, as well as its ability to continue in perpetuity and to shield the liability of its officers, directors and shareholders from the liability of the corporation.

Separate Legal Entity, Limiting Liability of Owners

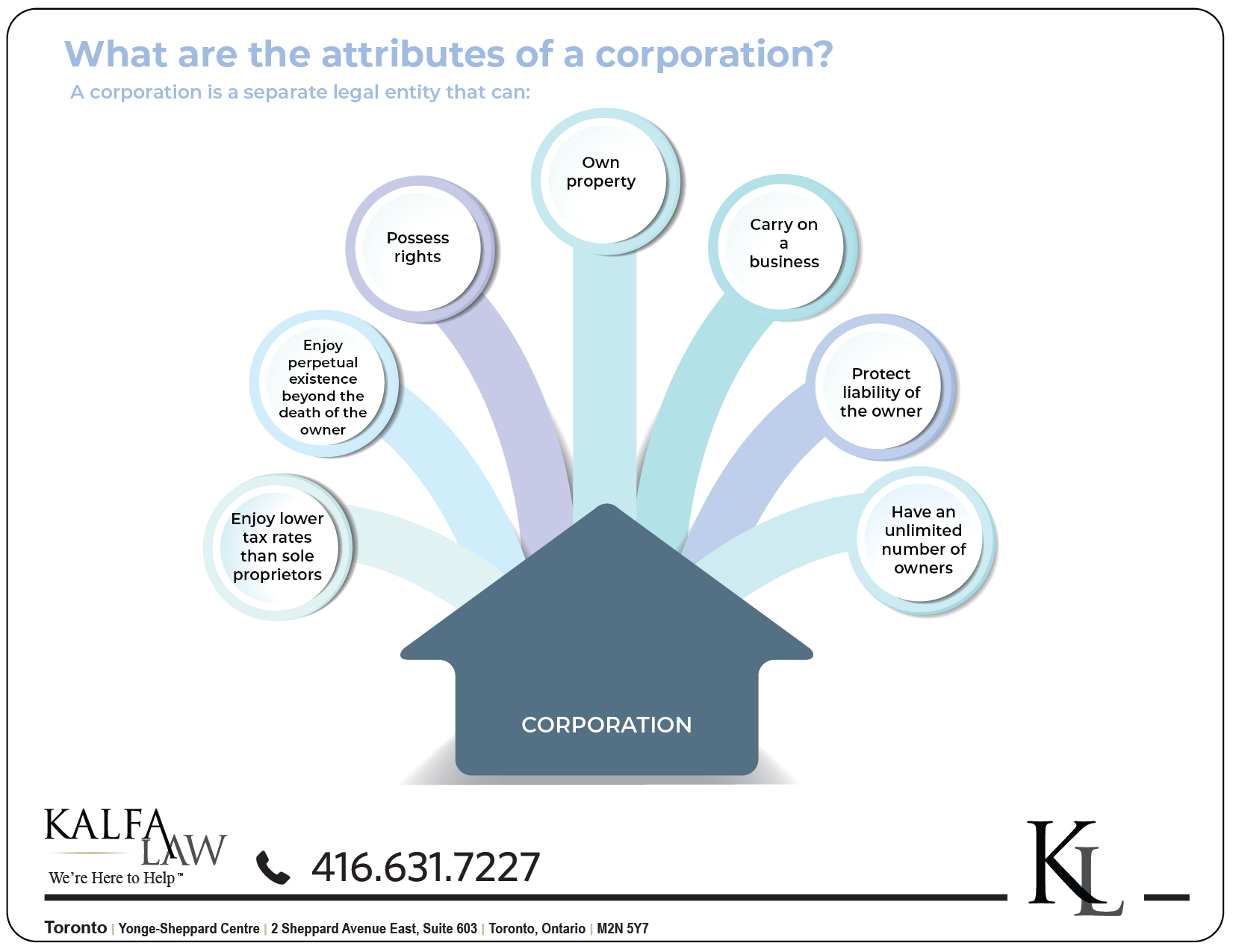

A Canadian corporation is a legal entity separate in law from its owners and can own property, carry on business, possess rights, and incur liabilities. Although the shareholders own the corporation through their ownership of shares, they do not own the property belonging to the corporation, and the rights and liabilities of the corporation are not the rights and liabilities of the shareholders.

If a business venture involves a great deal of risk, it is preferable to incorporate the business so as to isolate and protect the owner’s personal assets from corporate creditors and/or lawsuits. Sole proprietors are liable to the full extent of their personal assets for the liabilities of their businesses, whereas a shareholder’s liability to creditors of the corporation is limited to the amount of the shareholder’s investment. Directors are not liable at all (except where the Director engages in fraud).

Multiple Owners and Ease of Change of Ownership

Canadian corporations can potentially have an unlimited number of different owners. If the business has or is planning on having a number of owners, incorporation is preferable. It is also easier to transfer ownership in the business, as all the owners may simply sell their shares to another shareholder or sell them back to the Corporation. It is also easier to pass on the business to one’s next generation.

Perpetual Existence

Because corporations are distinct legal entities they enjoy perpetual existence. Partnerships and proprietorships cease to exist upon the death of a partner or the owner of a business. This can lead to undue hardship on the business at the time of death and the extreme difficulty of transferring the business to one’s next generation. In distinction, a corporation has a continual life of its own in spite of a death of shareholder/director of the incorporation. Therefore, substantial estate planning benefits result from this aspect of incorporation.

Tax Benefits

Although the foregoing considerations are significant when determining which form of carrying on business to select, unquestionably the most important and often the determining factor will be the impact of income tax on the business structure.

The income or loss of a business carried on by a corporation is both subject to tax at the level of the corporation, and the income is taxed again at the shareholder level once dividends are issued to the shareholders (owners) themselves.

Lower Tax Rates

Although this may seem like double taxation, less tax is still paid when the income is earned through a corporation. This occurs predominantly where the business is a Canadian Controlled Private Corporation (known as a CCPC and defined in s. 125(7) of the ITA) that earns Active Business Income (ABI), qualifying it for the Small Business Deduction (SBD).

Currently, a CCPC in Ontario is taxed at 11.5% on the first $500,000 of ABI in each year, which is 25.5% less than the combined average marginal personal tax rate. By way of comparison, a taxpayer in Ontario is taxed at a top marginal tax rate of 37.91% (combined federal and provincial rate) on income on income between $92,825 and 97,069. And an individual’s income is taxed at a top marginal tax rate of 48.19% (combined federal and provincial rate) on income between $150,473 and $214,368.

A corporation is thus taxed at a significantly lower tax rate than a sole proprietor. Incorporation allows the individual to pay taxes only on the amount he dividends out of the corporation to himself (essentially his income), while the retained earnings, or the ‘savings’ can remain in the corporation for future use, tax neutral.

Further, if all income earned by the corporation is paid out in the form of salary, the corporation will pay no income tax. The shareholders will be taxed at the same rate as if they had earned the income through a sole proprietorship or a partnership.

Sheltering Income With Lifetime Capital Gains Exemption

Finally, an added benefit of operating your business through a corporation is that you may take advantage of the Lifetime Capital Gains Exemption (LCGE), which in 2020 allows you to shelter $883,384 from taxes over the course of your lifetime when you sell the shares of the corporation. For more information on the LCGE and how you may take advantage of this excellent tax planning tool, read our article What is the Lifetime Capital Gains Exemption and How Can I Take Advantage of it?

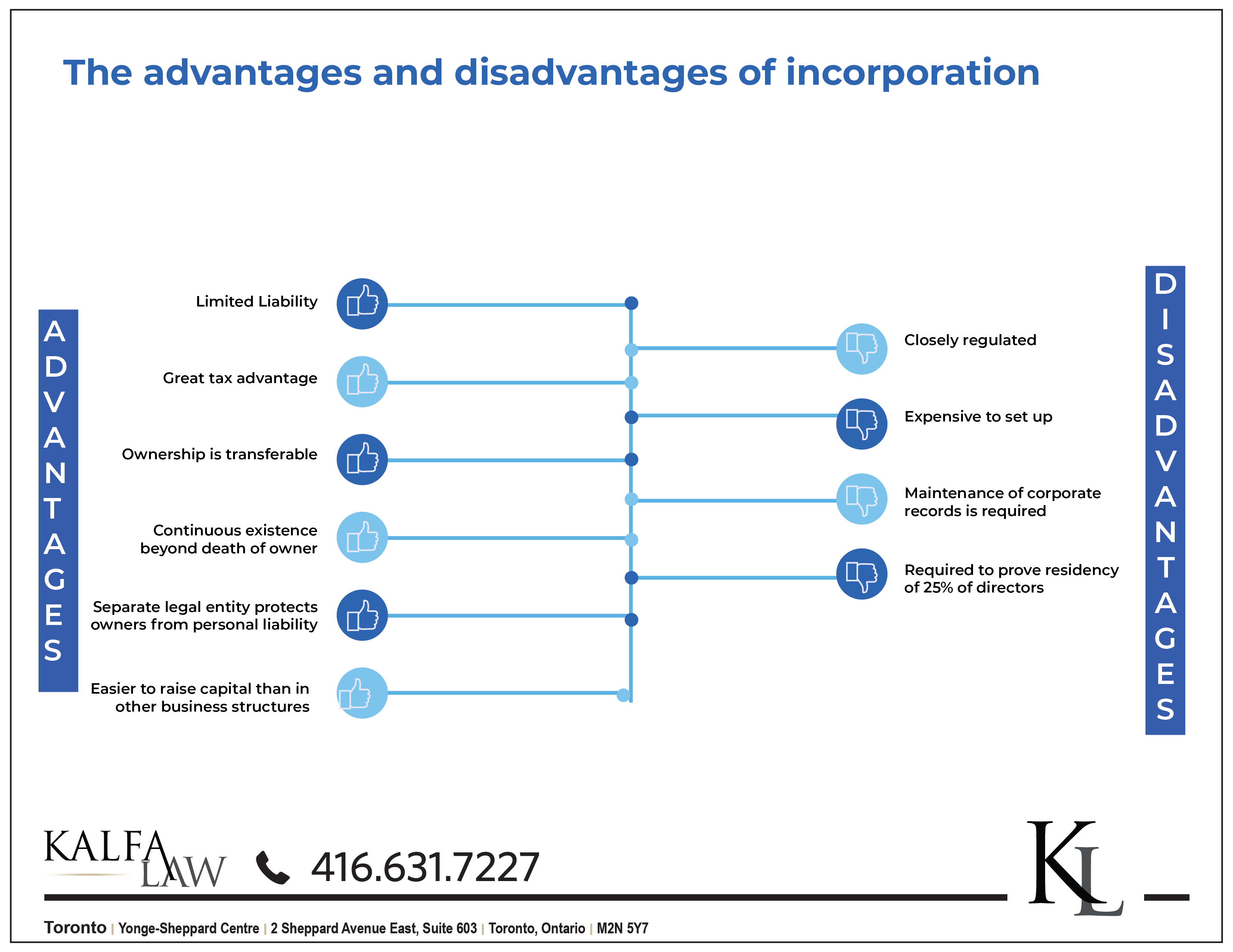

Summary of Advantages of Incorporating:

- Limited liability

- Ownership is transferable

- Continuous existence

- Separate legal entity

- Easier to raise capital than it might be with other business structures

- Many great tax advantages

Summary of Disadvantages of Incorporating:

- A corporation is closely regulated

- More expensive to set up a corporation than a sole proprietor; require use of an accountant

- Maintenance of corporate records is required, including documentation filed annually with the government

- You are required to prove residency or citizenship of directors

F.A.Qs:

For more information on the advantages and disadvantages selecting your business structure, Contact Us to speak with one of our business lawyers.

-Shira Kalfa, BA, JD, Partner and Founder

Shira Kalfa is the founding partner of Kalfa Law Firm. Shira’s practice is focused in corporate-commercial and tax law including corporate reorganizations, corporate restructuring, mergers and acquisitions, commercial financing, secured lending and transactional law. Shira graduated from York University achieving the highest academic accolade of Summa Cum Laude in 2012. She graduated from Western Law in 2015, with a specialization in business law. Shira is licensed to practice by the Law Society of Ontario. She is also a member of the Ontario Bar Association, the Canadian Tax Foundation, Women’s Law Association of Ontario, and the Toronto Jewish Law Society.

© Kalfa Law 2020

The above provides information of a general nature only. This does not constitute legal advice. All transactions or circumstances vary, and specified legal advice is required to meet your particular needs. If you have a legal question you should consult with a lawyer.